P002_WhatIsUniswap_Uniswap基本介绍

文档摘要

本节作者:@Web3Pignard 这一讲我们正式走进 Uniswap 的代码解析,准确来说是 Uniswap V3,通过阅读本节,你可以了解到: 什么是 Uniswap,Uniswap 推出了哪些版本,为什么要解析 V3 版本; Uniswap V3 由哪些合约构成,每个合约的主要功能和核心流程的解析。 解析 Uniswap 的代码可以帮助我们更好的理解后续的课程,当然你也可以直接跳转到后面的实战开发中,需要的时候再来查阅这一讲,但是我们还是建议你可以花一些时间学习一下 Uniswap 的代码实现,为后续的课程做准备。另外 Uniswap 的代码中会包含一些复杂的数学计算逻辑,可能不是很好理解,你也可以在后面的课程中持续学习。

本节作者:@Web3Pignard

这一讲我们正式走进 Uniswap 的代码解析,准确来说是 Uniswap V3,通过阅读本节,你可以了解到:

- 什么是 Uniswap,Uniswap 推出了哪些版本,为什么要解析 V3 版本;

- Uniswap V3 由哪些合约构成,每个合约的主要功能和核心流程的解析。

解析 Uniswap 的代码可以帮助我们更好的理解后续的课程,当然你也可以直接跳转到后面的实战开发中,需要的时候再来查阅这一讲,但是我们还是建议你可以花一些时间学习一下 Uniswap 的代码实现,为后续的课程做准备。另外 Uniswap 的代码中会包含一些复杂的数学计算逻辑,可能不是很好理解,你也可以在后面的课程中持续学习。如果你只是想要学习基础的去中心化应用开发,可以适当跳过那部分复杂的数学计算逻辑,我们的课程中也会直接使用 Uniswap V3 的一些代码库,降低课程的复杂度。

Uniswap 基本介绍

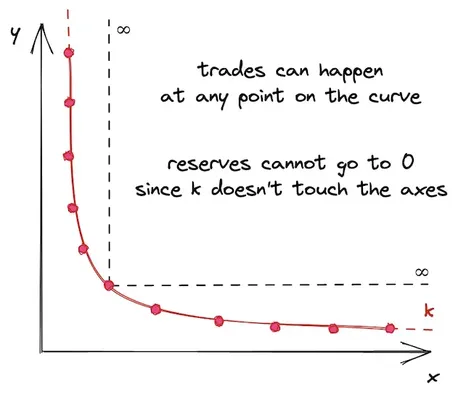

Uniswap 是以太坊上最大的去中心化交易所(DEX),我们在上一讲中提到了,Uniswap 这样的去中心化交易所采用的不是订单薄交易的方式,而是由 LP 提供流动性来交易,这个流动性池子中的代币如何定价则成为了去中心化交易所的关键。Uniswap 在其流动性池上构建了一种特定的自动做市商(AMM)机制。称为恒定乘积做市商(Constant Product Market Makers,CPMM)。顾名思义,其核心是一个非常简单的乘积公式:

流动性池是一个持有两种不同 token 的合约, x 和 y 分别代表 token0 的数目和 token1 的数目, k 是它们的乘积,当 swap 发生时,token0 和 token1 的数量都会发生变化,但二者乘积保持不变,仍然为 k 。

另外,我们一般说的 token0 的价格是指在流动性池中相对于 token1 的价格,价格与数量互为倒数,因此公式为:

就比如说我作为 LP 在池子中放了 1 个 ETH(token0) 和 3000 个 USDT(token1),那么 k 就是 1*3000=3000,ETH 价格就是 3000/1 = 3000U。那你作为交易方就可以把大概 30 USDT 放进去,拿出来 0.01 个 ETH。然后池子里面就变成了 3030 个 USDT 和 0.99 个 ETH,价格变 3030/0.99≈3030U。ETH 涨价了,这样是不是就解决了定价的问题,有人要换 ETH,ETH 变得稀缺,所以涨价了,下次要换 ETH 就需要更多的 USDT,只要保证池子中的 ETH * USDT 等于一个常量,这样自然就会此消彼长,当 ETH 变少时,你要通过 USDT 换取 ETH 时候就需要消耗更多 USDT,反之亦然。

当然上面的例子没有考虑滑点、手续费、取整等细节,实际合约实现时也有很多细节需要考虑。这里只是为了让大家理解基础逻辑,具体的细节会在后面展开。

Uniswap 到目前已经迭代了好几个版本,下面是各个版本的发展历程:

2018 年 11 月 Uniswap V1 发布,创新性地采用了上述 CPMM,支持 ERC-20 和 ETH 的兑换,为后续版本的 Uniswap 奠定了基础,并成为其他 AMM 协议的启示;

2020 年 5 月 Uniswap V2 发布, 在 V1 的基础上引入了 ERC-20 之间的兑换,以及时间加权平均价格(TWAP)预言机,增加交易对的灵活性,巩固了 Uniswap 在 DEX 的领先地位;

2021 年 5 月 Uniswap V3 发布,引入了集中流动性(Concentrated Liquidity),允许 LP 在交易对中定义特定的价格范围,以实现更精确的价格控制,提升了 LP 的资产利用率;

2023 年 6 月 Uniswap V4 公开了白皮书的草稿版本,引入了 Hook、Singleton、Flash Accounting 和原生 ETH 等多个优化,其中 Hook 是最重要的创新机制,给开发者提供了高度自定义性。

由于 Uniswap V4 截止目前(2024.05.11)尚未上线主网,并且其代码在 BSL 1.1 的许可下发布,该许可证将持续四年,并限制协议仅供经过治理批准的实体使用。虽然 V3 也使用 BSL 1.1 ,但许可证已于 2023 年 4 月 到期,因此本课程使用 V3 版本。

Uniswap V3 代码解析

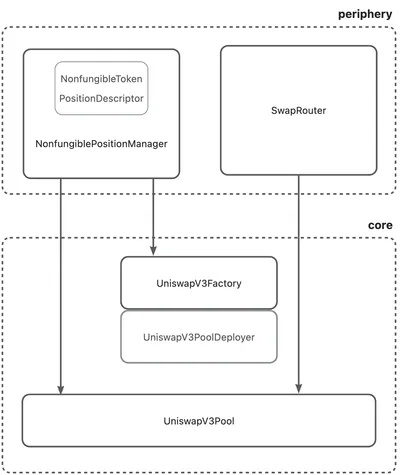

如上所说,Uniswap 核心就是要基于 CPMM 来实现一个自动化做市商,除了用户调用的交易合约外,还需要有提供给 LP 管理流动性池子的合约,以及对流动性的管理。这些功能在不同的合约中实现,在 Uniswap 的架构中,Uniswap V3 的合约大概被分为两类,分别存储在不同的仓库中:

- Uniswap v3-periphery:面向用户的接口代码,如头寸管理、swap 路由等功能,Uniswap 的前端界面与 periphery 合约交互,主要包含三个合约:

- NonfungiblePositionManager.sol:对应头寸管理功能,包含交易池(又称为流动性池或池子,后文统一用交易池表示)创建以及流动性的添加删除;

- NonfungibleTokenPositionDescriptor.sol:对头寸的描述信息;

- SwapRouter.sol:对应 swap 路由的功能,包含单交易池 swap 和多交易池 swap。

- Uniswap v3-core:Uniswap v3 的核心代码,实现了协议定义的所有功能,外部合约可直接与 core 合约交互,主要包含三个合约;

- UniswapV3Factory.sol:工厂合约,用来创建交易池,设置 Owner 和手续费等级;

- UniswapV3PoolDeployer.sol:工厂合约的基类,封装了部署交易池合约的功能;

- UniswapV3Pool.sol:交易池合约,持有实际的 Token,实现价格和流动性的管理,以及在当前交易池中 swap 的功能。

我们主要解析核心流程,包括以下:

- 部署交易池;

- 创建/添加/减少流动性;

- swap。

其中 1 和 2 都是合约提供给 LP 操作的功能,通过部署交易池和管理流动性来提供和管理流动性。而 3 则是提供给普通用户使用 Uniswap 的核心功能(甚至可以说是唯一的功能)swap,也就是交易。接下来我们讲依次讲解 Uniswap 中的相关代码。

部署交易池

在 Uniswap V3 中,通过合约 UniswapV3Pool 来定义一个交易池子,Uniswap 最核心的交易功能在最底层就是调用了该合约的 swap 方法。

而不同的交易对,以及不同的费率和价格区间(后面会具体讲到 tickSpacing)都会部署不同的 UniswapV3Pool 合约实例来负责交易。部署交易池则是针对某一对 token 以及指定费率的和价格区间来部署一个对应的交易池,当部署完成后再次出现同样条件下的交易池则不再需要重复部署了。

部署交易池调用的是 NonfungiblePositionManager 合约的 createAndInitializePoolIfNecessary,参数为:

- token0:token0 的地址,需要小于 token1 的地址且不为零地址;

- token1:token1 的地址;

- fee:以 1,000,000 为基底的手续费费率,Uniswap v3 前端界面支持四种手续费费率(0.01%,0.05%、0.30%、1.00%),对于一般的交易对推荐 0.30%,fee 取值即 3000;

- sqrtPriceX96:当前交易对价格的算术平方根左移 96 位的值,目的是为了方便合约中的计算。

代码为:

/// @inheritdoc IPoolInitializer function createAndInitializePoolIfNecessary( address token0, address token1, uint24 fee, uint160 sqrtPriceX96 ) external payable override returns (address pool) { require(token0 < token1); pool = IUniswapV3Factory(factory).getPool(token0, token1, fee); if (pool == address(0)) { pool = IUniswapV3Factory(factory).createPool(token0, token1, fee); IUniswapV3Pool(pool).initialize(sqrtPriceX96); } else { (uint160 sqrtPriceX96Existing, , , , , , ) = IUniswapV3Pool(pool).slot0(); if (sqrtPriceX96Existing == 0) { IUniswapV3Pool(pool).initialize(sqrtPriceX96); } } }

逻辑非常直观,首先将 token0,token1 和 fee 作为三元组取出交易池的地址 pool,如果取出的是零地址则创建交易池然后初始化,否则继续判断是否初始化过(当前价格),未初始化过则初始化。

我们分别看创建交易池的方法和初始化交易池的方法。

创建交易池

创建交易池调用的是 UniswapV3Factory 合约的 createPool,参数为:

- token0:token0 的地址

- token1 地址:token1 的地址;

- fee:手续费费率。

代码为:

/// @inheritdoc IUniswapV3Factory function createPool( address token0, address token1, uint24 fee ) external override noDelegateCall returns (address pool) { require(token0 != token1); (address token0, address token1) = token0 < token1 ? (token0, token1) : (token1, token0); require(token0 != address(0)); int24 tickSpacing = feeAmountTickSpacing[fee]; require(tickSpacing != 0); require(getPool[token0][token1][fee] == address(0)); pool = deploy(address(this), token0, token1, fee, tickSpacing); getPool[token0][token1][fee] = pool; // populate mapping in the reverse direction, deliberate choice to avoid the cost of comparing addresses getPool[token1][token0][fee] = pool; emit PoolCreated(token0, token1, fee, tickSpacing, pool); }

通过 fee 获取对应的 tickSpacing,要解释 tickSpacing 必须先解释 tick。

int24 tickSpacing = feeAmountTickSpacing[fee];

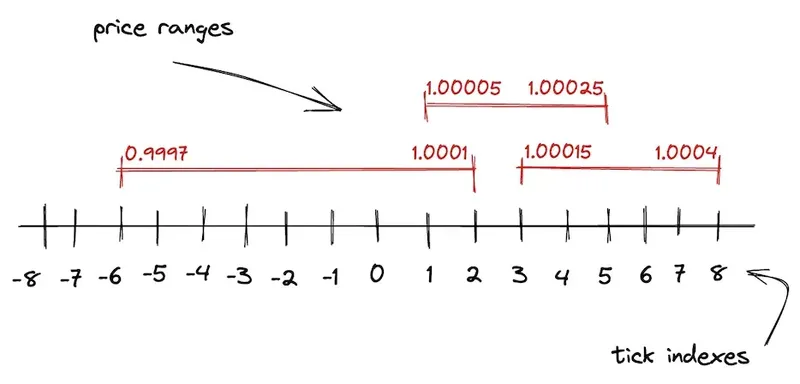

tick 是 V3 中价格的表示,如下图所示:

在 V3,整个价格区间由离散的、均匀分布的 ticks 进行标定。因为在 Uniswap V3 中 LP 添加流动性时都会提供一个价格的范围(为了 LP 可以更好的管理头寸),要让不同价格范围的流动性可以更好的管理和利用,需要 ticks 来将价格划分为一个一个的区间,每个 tick 有一个 index 和对应的价格:

P(i) 即为 tick 在 i 位置的价格. 后一个价格点的价格是前一个价格点价格基础上浮动万分之一。我们可以得到关于 i 的公式:

V3 规定只有被 tickSpacing 整除的 tick 才允许被初始化,tickSpacing 越大,每个 tick 流动性越多,tick 之间滑点越大,但会节省跨 tick 操作的 gas。

随后确认对应的交易池合约尚未被创建,调用 deploy,参数为工厂合约地址,token0 地址,token1 地址,fee,以及上面提到的 tickSpacing。

pool = deploy(address(this), token0, token1, fee, tickSpacing);

deploy 的代码如下:

/// @dev Deploys a pool with the given parameters by transiently setting the parameters storage slot and then /// clearing it after deploying the pool. /// @param factory The contract address of the Uniswap V3 factory /// @param token0 The first token of the pool by address sort order /// @param token1 The second token of the pool by address sort order /// @param fee The fee collected upon every swap in the pool, denominated in hundredths of a bip /// @param tickSpacing The spacing between usable ticks function deploy( address factory, address token0, address token1, uint24 fee, int24 tickSpacing ) internal returns (address pool) { parameters = Parameters({factory: factory, token0: token0, token1: token1, fee: fee, tickSpacing: tickSpacing}); pool = address(new UniswapV3Pool{salt: keccak256(abi.encode(token0, token1, fee))}()); delete parameters; }

deploy 方法会先临时存储交易池合约初始化参数 parameters ,临时存储 parameters 的目的是为了让交易池合约的构造方法反向获取工厂合约的 parameters 变量从而完成参数的传递。

交易池合约的构造方法代码如下:

constructor() { int24 _tickSpacing; (factory, token0, token1, fee, _tickSpacing) = IUniswapV3PoolDeployer(msg.sender).parameters(); tickSpacing = _tickSpacing; maxLiquidityPerTick = Tick.tickSpacingToMaxLiquidityPerTick(_tickSpacing); }

回到 deploy,然后使用 new 方法中传递 salt 参数实现 CREATE2 操作码创建交易池合约,使用 CREATE2 的目的是确保相同 token0,token1 和 fee 能计算出相同且唯一的地址。

最后,保存交易池合约地址到 getPool 变量中:

getPool[token0][token1][fee] = pool; // populate mapping in the reverse direction, deliberate choice to avoid the cost of comparing addresses getPool[token1][token0][fee] = pool;

至此完成了交易池合约的创建。

初始化交易池

初始化交易池调用的是 UniswapV3Factory 合约的 initialize,参数为当前价格 sqrtPriceX96,含义上面已经介绍过了。

代码如下:

/// @inheritdoc IUniswapV3PoolActions /// @dev not locked because it initializes unlocked function initialize(uint160 sqrtPriceX96) external override { require(slot0.sqrtPriceX96 == 0, 'AI'); int24 tick = TickMath.getTickAtSqrtRatio(sqrtPriceX96); (uint16 cardinality, uint16 cardinalityNext) = observations.initialize(_blockTimestamp()); slot0 = Slot0({ sqrtPriceX96: sqrtPriceX96, tick: tick, observationIndex: 0, observationCardinality: cardinality, observationCardinalityNext: cardinalityNext, feeProtocol: 0, unlocked: true }); emit Initialize(sqrtPriceX96, tick); }

首先从 sqrtPriceX96 换算出 tick 的值。

int24 tick = TickMath.getTickAtSqrtRatio(sqrtPriceX96);

然后初始化预言机,cardinality 表示当前预言机的观测点数组容量, cardinalityNext 表示预言机扩容后的观测点数组容量,这里不详细解释。

(uint16 cardinality, uint16 cardinalityNext) = observations.initialize(_blockTimestamp());

最后初始化 slot0 变量,用于记录交易池的全局状态,这里主要就是记录价格和预言机的状态。

slot0 = Slot0({ sqrtPriceX96: sqrtPriceX96, tick: tick, observationIndex: 0, observationCardinality: cardinality, observationCardinalityNext: cardinalityNext, feeProtocol: 0, unlocked: true });

Slot0结构如下,源码中已经有了详细的注释。

struct Slot0 { // the current price uint160 sqrtPriceX96; // the current tick int24 tick; // the most-recently updated index of the observations array uint16 observationIndex; // the current maximum number of observations that are being stored uint16 observationCardinality; // the next maximum number of observations to store, triggered in observations.write uint16 observationCardinalityNext; // the current protocol fee as a percentage of the swap fee taken on withdrawal // represented as an integer denominator (1/x)% uint8 feeProtocol; // whether the pool is locked bool unlocked; }

至此完成了交易池合约的初始化。

创建/添加/减少流动性

创建/添加/减少流动性也就是对应 Uniswap 的 UI 中 https://app.uniswap.org/pool 这部分页面的操作内容,是提供给 LP 管理流动性的功能。

创建流动性

创建流动性调用的是 NonfungiblePositionManager 合约的 mint。

参数如下:

struct MintParams { address token0; // token0 地址 address token1; // token1 地址 uint24 fee; // 费率 int24 tickLower; // 流动性区间下界 int24 tickUpper; // 流动性区间上界 uint256 amount0Desired; // 添加流动性中 token0 数量 uint256 amount1Desired; // 添加流动性中 token1 数量 uint256 amount0Min; // 最小添加 token0 数量 uint256 amount1Min; // 最小添加 token1 数量 address recipient; // 头寸接受者的地址 uint256 deadline; // 过期的区块号 }

代码如下:

/// @inheritdoc INonfungiblePositionManager function mint(MintParams calldata params) external payable override checkDeadline(params.deadline) returns ( uint256 tokenId, uint128 liquidity, uint256 amount0, uint256 amount1 ) { IUniswapV3Pool pool; (liquidity, amount0, amount1, pool) = addLiquidity( AddLiquidityParams({ token0: params.token0, token1: params.token1, fee: params.fee, recipient: address(this), tickLower: params.tickLower, tickUpper: params.tickUpper, amount0Desired: params.amount0Desired, amount1Desired: params.amount1Desired, amount0Min: params.amount0Min, amount1Min: params.amount1Min }) ); _mint(params.recipient, (tokenId = _nextId++)); bytes32 positionKey = PositionKey.compute(address(this), params.tickLower, params.tickUpper); (, uint256 feeGrowthInside0LastX128, uint256 feeGrowthInside1LastX128, , ) = pool.positions(positionKey); // idempotent set uint80 poolId = cachePoolKey( address(pool), PoolAddress.PoolKey({token0: params.token0, token1: params.token1, fee: params.fee}) ); _positions[tokenId] = Position({ nonce: 0, operator: address(0), poolId: poolId, tickLower: params.tickLower, tickUpper: params.tickUpper, liquidity: liquidity, feeGrowthInside0LastX128: feeGrowthInside0LastX128, feeGrowthInside1LastX128: feeGrowthInside1LastX128, tokensOwed0: 0, tokensOwed1: 0 }); emit IncreaseLiquidity(tokenId, liquidity, amount0, amount1); }

梳理下整体逻辑,首先是 addLiquidity 添加流动性,然后调用 _mint 发送凭证(NFT)给头寸接受者,接着计算一个自增的 poolId,跟交易池地址互相索引,最后将所有信息记录到头寸的结构体中。

addLiquidity 方法定义在这里,核心是计算出 liquidity 然后调用交易池合约 mint 方法。

(amount0, amount1) = pool.mint( params.recipient, params.tickLower, params.tickUpper, liquidity, abi.encode(MintCallbackData({poolKey: poolKey, payer: msg.sender})) );

liquidity ,即流动性,跟 tick 一样,也是 V3 中的重要概念。

在 V2 中,如果我们设定乘积 k = L^2, L 就是我们常说的流动性,得出如下公式:

V2 流动性池的流动性是分布在 0 到正无穷,如下图所示:

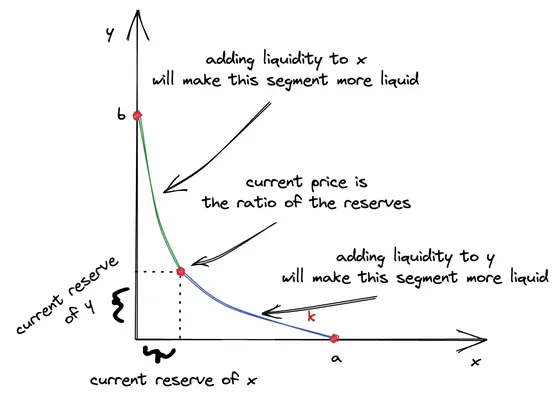

在 v3 中,每个头寸提供了一个价格区间,假设 token0 的价格在价格上界 a 和价格下界 b 之间波动,为了实现集中流动性,那么曲线必须在 x/y 轴进行平移,使得 a/b 点和 x/y 轴重合,如下图:

我们忽略推导过程,直接给出数学公式:

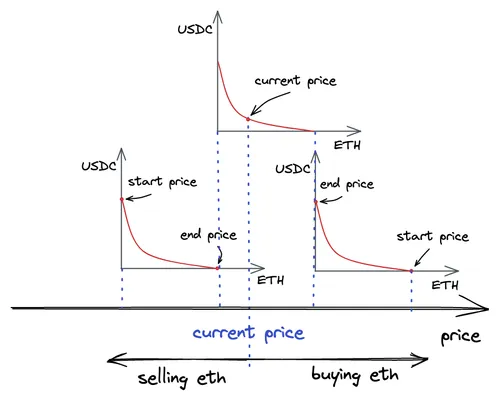

我们将图中的曲线分为两部分:起始点左边和起始点右边。在swap过程中,当前价格会朝着某个方向移动:升高或降低。对于价格的移动,仅有一种 token 会起作用:当前价格升高时,swap仅需要 token0;当前价格降低时,swap仅需要 token1。

当流动性提供者提供了 \Delta{x} 个 token0 时,意味着向起始点左边添加了如下流动性:

当流动性提供者提供了 \Delta{y} 个 token1 时,意味着向起始点右边添加了如下流动性:

如果当前价格超过价格区间属于只能添加单边流动性的情况。

当前价格小于下界 b 时,只有 \Delta{y} 个 token1 起作用,意味着向 b 点右边添加了如下流动性:

当前价格大于上界 a 时,只有 \Delta{x} 个 token0 起作用,意味着向 a 点左边添加了如下流动性:

回到代码,计算 liquidity 的步骤如下:

- 如果价格在价格区间内,分别计算出两边流动性然后取最小值;

- 如果当前价格超过价格区间则是计算出单边流动性。

交易池合约的 mint方法。

参数为:

- recipient:头寸接收者地址

- tickLower:流动性区间下界

- tickUpper:流动性区间上界

- amount:流动性数量

- data:回调参数

代码为:

/// @inheritdoc IUniswapV3PoolActions /// @dev noDelegateCall is applied indirectly via _modifyPosition function mint( address recipient, int24 tickLower, int24 tickUpper, uint128 amount, bytes calldata data ) external override lock returns (uint256 amount0, uint256 amount1) { require(amount > 0); (, int256 amount0Int, int256 amount1Int) = _modifyPosition( ModifyPositionParams({ owner: recipient, tickLower: tickLower, tickUpper: tickUpper, liquidityDelta: int256(amount).toInt128() }) ); amount0 = uint256(amount0Int); amount1 = uint256(amount1Int); uint256 balance0Before; uint256 balance1Before; if (amount0 > 0) balance0Before = balance0(); if (amount1 > 0) balance1Before = balance1(); IUniswapV3MintCallback(msg.sender).uniswapV3MintCallback(amount0, amount1, data); if (amount0 > 0) require(balance0Before.add(amount0) <= balance0(), 'M0'); if (amount1 > 0) require(balance1Before.add(amount1) <= balance1(), 'M1'); emit Mint(msg.sender, recipient, tickLower, tickUpper, amount, amount0, amount1); }

首先调用 _modifyPosition 方法修改当前价格区间的流动性,这个方法相对复杂,放到后面专门讲。其返回的 amount0Int 和 amount1Int 表示 amount 流动性对应的 token0 和 token1 的代币数量。

调用 mint 方法的合约需要实现 IUniswapV3MintCallback 接口完成代币的转入操作:

IUniswapV3MintCallback(msg.sender).uniswapV3MintCallback(amount0, amount1, data);

IUniswapV3MintCallback 的实现在 periphery 仓库的 LiquidityManagement.sol 中。目的是通知调用方向交易池合约转入 amount0 个 token0 和 amount1 个 token2。

/// @inheritdoc IUniswapV3MintCallback function uniswapV3MintCallback( uint256 amount0Owed, uint256 amount1Owed, bytes calldata data ) external override { MintCallbackData memory decoded = abi.decode(data, (MintCallbackData)); CallbackValidation.verifyCallback(factory, decoded.poolKey); if (amount0Owed > 0) pay(decoded.poolKey.token0, decoded.payer, msg.sender, amount0Owed); if (amount1Owed > 0) pay(decoded.poolKey.token1, decoded.payer, msg.sender, amount1Owed); }

回调完成后会检查交易池合约的对应余额是否发生变化,并且增量应该大于 amount0 和 amount1:这意味着调用方确实转入了所需的资产。

if (amount0 > 0) require(balance0Before.add(amount0) <= balance0(), 'M0'); if (amount1 > 0) require(balance1Before.add(amount1) <= balance1(), 'M1');

至此完成了流动性的创建。

添加流动性

添加流动性调用的是 NonfungiblePositionManager 合约的 increaseLiquidity。

参数如下:

struct IncreaseLiquidityParams { uint256 tokenId; // 头寸 id uint256 amount0Desired; // 添加流动性中 token0 数量 uint256 amount1Desired; // 添加流动性中 token1 数量 uint256 amount0Min; // 最小添加 token0 数量 uint256 amount1Min; // 最小添加 token1 数量 uint256 deadline; // 过期的区块号 }

代码如下:

/// @inheritdoc INonfungiblePositionManager function increaseLiquidity(IncreaseLiquidityParams calldata params) external payable override checkDeadline(params.deadline) returns ( uint128 liquidity, uint256 amount0, uint256 amount1 ) { Position storage position = _positions[params.tokenId]; PoolAddress.PoolKey memory poolKey = _poolIdToPoolKey[position.poolId]; IUniswapV3Pool pool; (liquidity, amount0, amount1, pool) = addLiquidity( AddLiquidityParams({ token0: poolKey.token0, token1: poolKey.token1, fee: poolKey.fee, tickLower: position.tickLower, tickUpper: position.tickUpper, amount0Desired: params.amount0Desired, amount1Desired: params.amount1Desired, amount0Min: params.amount0Min, amount1Min: params.amount1Min, recipient: address(this) }) ); bytes32 positionKey = PositionKey.compute(address(this), position.tickLower, position.tickUpper); // this is now updated to the current transaction (, uint256 feeGrowthInside0LastX128, uint256 feeGrowthInside1LastX128, , ) = pool.positions(positionKey); position.tokensOwed0 += uint128( FullMath.mulDiv( feeGrowthInside0LastX128 - position.feeGrowthInside0LastX128, position.liquidity, FixedPoint128.Q128 ) ); position.tokensOwed1 += uint128( FullMath.mulDiv( feeGrowthInside1LastX128 - position.feeGrowthInside1LastX128, position.liquidity, FixedPoint128.Q128 ) ); position.feeGrowthInside0LastX128 = feeGrowthInside0LastX128; position.feeGrowthInside1LastX128 = feeGrowthInside1LastX128; position.liquidity += liquidity; emit IncreaseLiquidity(params.tokenId, liquidity, amount0, amount1); }

整体逻辑跟 mint 类似,先从 tokeinId 拿到头寸,然后 addLiquidity 添加流动性,返回添加成功的流动性 liquidity,所消耗的 amount0 和 amount1,以及交易池合约 pool。根据 pool 对象里的最新头寸信息,更新头寸状态。

减少流动性

减少流动性调用的是 NonfungiblePositionManager 合约的 decreaseLiquidity。

参数如下:

struct DecreaseLiquidityParams { uint256 tokenId; // 头寸 id uint128 liquidity; // 减少流动性数量 uint256 amount0Min; // 最小减少 token0 数量 uint256 amount1Min; // 最小减少 token1 数量 uint256 deadline; // 过期的区块号 }

代码如下:

/// @inheritdoc INonfungiblePositionManager function decreaseLiquidity(DecreaseLiquidityParams calldata params) external payable override isAuthorizedForToken(params.tokenId) checkDeadline(params.deadline) returns (uint256 amount0, uint256 amount1) { require(params.liquidity > 0); Position storage position = _positions[params.tokenId]; uint128 positionLiquidity = position.liquidity; require(positionLiquidity >= params.liquidity); PoolAddress.PoolKey memory poolKey = _poolIdToPoolKey[position.poolId]; IUniswapV3Pool pool = IUniswapV3Pool(PoolAddress.computeAddress(factory, poolKey)); (amount0, amount1) = pool.burn(position.tickLower, position.tickUpper, params.liquidity); require(amount0 >= params.amount0Min && amount1 >= params.amount1Min, 'Price slippage check'); bytes32 positionKey = PositionKey.compute(address(this), position.tickLower, position.tickUpper); // this is now updated to the current transaction (, uint256 feeGrowthInside0LastX128, uint256 feeGrowthInside1LastX128, , ) = pool.positions(positionKey); position.tokensOwed0 += uint128(amount0) + uint128( FullMath.mulDiv( feeGrowthInside0LastX128 - position.feeGrowthInside0LastX128, positionLiquidity, FixedPoint128.Q128 ) ); position.tokensOwed1 += uint128(amount1) + uint128( FullMath.mulDiv( feeGrowthInside1LastX128 - position.feeGrowthInside1LastX128, positionLiquidity, FixedPoint128.Q128 ) ); position.feeGrowthInside0LastX128 = feeGrowthInside0LastX128; position.feeGrowthInside1LastX128 = feeGrowthInside1LastX128; // subtraction is safe because we checked positionLiquidity is gte params.liquidity position.liquidity = positionLiquidity - params.liquidity; emit DecreaseLiquidity(params.tokenId, params.liquidity, amount0, amount1); }

跟 increaseLiquidity 是反向操作,核心逻辑是调用交易池合约的 burn 方法。

(amount0, amount1) = pool.burn(position.tickLower, position.tickUpper, params.liquidity);

burn 的参数为流动性区间下界 tickLower,流动性区间上界 tickUpper 和流动性数量 amount,代码如下:

/// @inheritdoc IUniswapV3PoolActions /// @dev noDelegateCall is applied indirectly via _modifyPosition function burn( int24 tickLower, int24 tickUpper, uint128 amount ) external override lock returns (uint256 amount0, uint256 amount1) { (Position.Info storage position, int256 amount0Int, int256 amount1Int) = _modifyPosition( ModifyPositionParams({ owner: msg.sender, tickLower: tickLower, tickUpper: tickUpper, liquidityDelta: -int256(amount).toInt128() }) ); amount0 = uint256(-amount0Int); amount1 = uint256(-amount1Int); if (amount0 > 0 || amount1 > 0) { (position.tokensOwed0, position.tokensOwed1) = ( position.tokensOwed0 + uint128(amount0), position.tokensOwed1 + uint128(amount1) ); } emit Burn(msg.sender, tickLower, tickUpper, amount, amount0, amount1); }

也是调用 _modifyPosition 方法修改当前价格区间的流动性,返回的 amount0Int 和 amount1Int 表示 amount 流动性对应的 token0 和 token1 的代币数量,position 表示用户的头寸信息,在这里主要作用是用来记录待取回代币数量。

if (amount0 > 0 || amount1 > 0) { (position.tokensOwed0, position.tokensOwed1) = ( position.tokensOwed0 + uint128(amount0), position.tokensOwed1 + uint128(amount1) ); }

用户可以通过主动调用 collect 方法取出自己头寸信息记录的 tokensOwed0 数量的 token0 和 tokensOwed1 数量对应的 token1。

collect 方法在下一节展开。

collect

取出待领取代币调用的是 NonfungiblePositionManager 合约的 collect。

参数如下:

struct CollectParams { uint256 tokenId; // 头寸 id address recipient; // 接收者地址 uint128 amount0Max; // 最大 token0 数量 uint128 amount1Max; // 最大 token1 数量 }

代码如下:

/// @inheritdoc INonfungiblePositionManager function collect(CollectParams calldata params) external payable override isAuthorizedForToken(params.tokenId) returns (uint256 amount0, uint256 amount1) { require(params.amount0Max > 0 || params.amount1Max > 0); // allow collecting to the nft position manager address with address 0 address recipient = params.recipient == address(0) ? address(this) : params.recipient; Position storage position = _positions[params.tokenId]; PoolAddress.PoolKey memory poolKey = _poolIdToPoolKey[position.poolId]; IUniswapV3Pool pool = IUniswapV3Pool(PoolAddress.computeAddress(factory, poolKey)); (uint128 tokensOwed0, uint128 tokensOwed1) = (position.tokensOwed0, position.tokensOwed1); // trigger an update of the position fees owed and fee growth snapshots if it has any liquidity if (position.liquidity > 0) { pool.burn(position.tickLower, position.tickUpper, 0); (, uint256 feeGrowthInside0LastX128, uint256 feeGrowthInside1LastX128, , ) = pool.positions(PositionKey.compute(address(this), position.tickLower, position.tickUpper)); tokensOwed0 += uint128( FullMath.mulDiv( feeGrowthInside0LastX128 - position.feeGrowthInside0LastX128, position.liquidity, FixedPoint128.Q128 ) ); tokensOwed1 += uint128( FullMath.mulDiv( feeGrowthInside1LastX128 - position.feeGrowthInside1LastX128, position.liquidity, FixedPoint128.Q128 ) ); position.feeGrowthInside0LastX128 = feeGrowthInside0LastX128; position.feeGrowthInside1LastX128 = feeGrowthInside1LastX128; } // compute the arguments to give to the pool#collect method (uint128 amount0Collect, uint128 amount1Collect) = ( params.amount0Max > tokensOwed0 ? tokensOwed0 : params.amount0Max, params.amount1Max > tokensOwed1 ? tokensOwed1 : params.amount1Max ); // the actual amounts collected are returned (amount0, amount1) = pool.collect( recipient, position.tickLower, position.tickUpper, amount0Collect, amount1Collect ); // sometimes there will be a few less wei than expected due to rounding down in core, but we just subtract the full amount expected // instead of the actual amount so we can burn the token (position.tokensOwed0, position.tokensOwed1) = (tokensOwed0 - amount0Collect, tokensOwed1 - amount1Collect); emit Collect(params.tokenId, recipient, amount0Collect, amount1Collect); }

首先获取待取回代币数量,如果该头寸含有流动性,则触发一次头寸状态的更新,这里调用了交易池合约的burn方法,但是传入的流动性参数为 0。这是因为 V3 只在 mint 和 burn 时才更新头寸状态,而 collect 方法可能在 swap 之后被调用,可能会导致头寸状态不是最新的。最后调用了交易池合约的 collect 方法取回代币。

// the actual amounts collected are returned (amount0, amount1) = pool.collect( recipient, position.tickLower, position.tickUpper, amount0Collect, amount1Collect );

交易池合约的 collect 的逻辑比较简单,这里就不展开了,参数 amount0Requested 为请求取回 token0 的数量,amount1Requested 即请求取回 token1 的数量。如果 amount0Requested 大于 position.tokensOwed0,则取回所有的 token0,取回 token1 也同理。

_modifyPosition

_modifyPosition 方法是 mint 和 burn 的核心方法。

参数如下:

struct ModifyPositionParams { // the address that owns the position address owner; // the lower and upper tick of the position int24 tickLower; int24 tickUpper; // any change in liquidity int128 liquidityDelta; }

代码如下:

/// @dev Effect some changes to a position /// @param params the position details and the change to the position's liquidity to effect /// @return position a storage pointer referencing the position with the given owner and tick range /// @return amount0 the amount of token0 owed to the pool, negative if the pool should pay the recipient /// @return amount1 the amount of token1 owed to the pool, negative if the pool should pay the recipient function _modifyPosition(ModifyPositionParams memory params) private noDelegateCall returns ( Position.Info storage position, int256 amount0, int256 amount1 ) { checkTicks(params.tickLower, params.tickUpper); Slot0 memory _slot0 = slot0; // SLOAD for gas optimization position = _updatePosition( params.owner, params.tickLower, params.tickUpper, params.liquidityDelta, _slot0.tick ); if (params.liquidityDelta != 0) { if (_slot0.tick < params.tickLower) { // current tick is below the passed range; liquidity can only become in range by crossing from left to // right, when we'll need _more_ token0 (it's becoming more valuable) so user must provide it amount0 = SqrtPriceMath.getAmount0Delta( TickMath.getSqrtRatioAtTick(params.tickLower), TickMath.getSqrtRatioAtTick(params.tickUpper), params.liquidityDelta ); } else if (_slot0.tick < params.tickUpper) { // current tick is inside the passed range uint128 liquidityBefore = liquidity; // SLOAD for gas optimization // write an oracle entry (slot0.observationIndex, slot0.observationCardinality) = observations.write( _slot0.observationIndex, _blockTimestamp(), _slot0.tick, liquidityBefore, _slot0.observationCardinality, _slot0.observationCardinalityNext ); amount0 = SqrtPriceMath.getAmount0Delta( _slot0.sqrtPriceX96, TickMath.getSqrtRatioAtTick(params.tickUpper), params.liquidityDelta ); amount1 = SqrtPriceMath.getAmount1Delta( TickMath.getSqrtRatioAtTick(params.tickLower), _slot0.sqrtPriceX96, params.liquidityDelta ); liquidity = LiquidityMath.addDelta(liquidityBefore, params.liquidityDelta); } else { // current tick is above the passed range; liquidity can only become in range by crossing from right to // left, when we'll need _more_ token1 (it's becoming more valuable) so user must provide it amount1 = SqrtPriceMath.getAmount1Delta( TickMath.getSqrtRatioAtTick(params.tickLower), TickMath.getSqrtRatioAtTick(params.tickUpper), params.liquidityDelta ); } } }

先通过 _updatePosition 更新头寸信息,接着分别计算出 liquidityDelta 流动性需要提供的 token0 数量 amount0 和 token1 数量 amount1,流动性的计算公式在创建流动性时已经介绍了。

_updatePosition 方法代码如下:

/// @dev Gets and updates a position with the given liquidity delta /// @param owner the owner of the position /// @param tickLower the lower tick of the position's tick range /// @param tickUpper the upper tick of the position's tick range /// @param tick the current tick, passed to avoid sloads function _updatePosition( address owner, int24 tickLower, int24 tickUpper, int128 liquidityDelta, int24 tick ) private returns (Position.Info storage position) { position = positions.get(owner, tickLower, tickUpper); uint256 _feeGrowthGlobal0X128 = feeGrowthGlobal0X128; // SLOAD for gas optimization uint256 _feeGrowthGlobal1X128 = feeGrowthGlobal1X128; // SLOAD for gas optimization // if we need to update the ticks, do it bool flippedLower; bool flippedUpper; if (liquidityDelta != 0) { uint32 time = _blockTimestamp(); (int56 tickCumulative, uint160 secondsPerLiquidityCumulativeX128) = observations.observeSingle( time, 0, slot0.tick, slot0.observationIndex, liquidity, slot0.observationCardinality ); flippedLower = ticks.update( tickLower, tick, liquidityDelta, _feeGrowthGlobal0X128, _feeGrowthGlobal1X128, secondsPerLiquidityCumulativeX128, tickCumulative, time, false, maxLiquidityPerTick ); flippedUpper = ticks.update( tickUpper, tick, liquidityDelta, _feeGrowthGlobal0X128, _feeGrowthGlobal1X128, secondsPerLiquidityCumulativeX128, tickCumulative, time, true, maxLiquidityPerTick ); if (flippedLower) { tickBitmap.flipTick(tickLower, tickSpacing); } if (flippedUpper) { tickBitmap.flipTick(tickUpper, tickSpacing); } } (uint256 feeGrowthInside0X128, uint256 feeGrowthInside1X128) = ticks.getFeeGrowthInside(tickLower, tickUpper, tick, _feeGrowthGlobal0X128, _feeGrowthGlobal1X128); position.update(liquidityDelta, feeGrowthInside0X128, feeGrowthInside1X128); // clear any tick data that is no longer needed if (liquidityDelta < 0) { if (flippedLower) { ticks.clear(tickLower); } if (flippedUpper) { ticks.clear(tickUpper); } } }

ticktickCumulative 和 secondsPerLiquidityCumulativeX128 是预言机观察点相关的两个变量,这里不详细解释。

(int56 tickCumulative, uint160 secondsPerLiquidityCumulativeX128) = observations.observeSingle( time, 0, slot0.tick, slot0.observationIndex, liquidity, slot0.observationCardinality );

接着使用 ticks.update 分别更新价格区间低点和价格区间高点的状态。如果对应 tick 的流动性从从无到有,或从有到无,则表示该 tick 需要被翻转。

flippedLower = ticks.update( tickLower, tick, liquidityDelta, _feeGrowthGlobal0X128, _feeGrowthGlobal1X128, secondsPerLiquidityCumulativeX128, tickCumulative, time, false, maxLiquidityPerTick ); flippedUpper = ticks.update( tickUpper, tick, liquidityDelta, _feeGrowthGlobal0X128, _feeGrowthGlobal1X128, secondsPerLiquidityCumulativeX128, tickCumulative, time, true, maxLiquidityPerTick );

随后计算该价格区间的累积的流动性手续费。

(uint256 feeGrowthInside0X128, uint256 feeGrowthInside1X128) = ticks.getFeeGrowthInside(tickLower, tickUpper, tick, _feeGrowthGlobal0X128, _feeGrowthGlobal1X128);

最后更新头寸信息,并判断是否 tick 被翻转,如果 tick 被翻转则调用 ticks.clear 清空 tick 状态。

position.update(liquidityDelta, feeGrowthInside0X128, feeGrowthInside1X128); // clear any tick data that is no longer needed if (liquidityDelta < 0) { if (flippedLower) { } if (flippedUpper) { ticks.clear(tickUpper); } }

至此完成更新头寸流程。

swap

swap 也就指交易,是 Uniswap 中最常用的也是最核心的功能。对应 https://app.uniswap.org/swap 中的相关操作,接下来让我们看看 Uniswap 的合约是如何实现 swap 的。

SwapRouter 合约包含了以下四个交换代币的方法:

exactInput:多池交换,用户指定输入代币数量,尽可能多地获得输出代币;exactInputSingle:单池交换,用户指定输入代币数量,尽可能多地获得输出代币;exactOutput:多池交换,用户指定输出代币数量,尽可能少地提供输入代币;exactOutputSingle:单池交换,用户指定输出代币数量,尽可能少地提供输入代币。

这里分成"指定输入代币数量"和"指定输出代币数量"分别介绍。

指定输入代币数量

exactInput 方法负责多池交换,指定 swap 路径以及输入代币数量,尽可能多地获得输出代币。

参数如下:

struct ExactInputParams { bytes path; // swap 路径,可以解析成一个或多个交易池 address recipient; // 接收者地址 uint256 deadline; // 过期的区块号 uint256 amountIn; // 输入代币数量 uint256 amountOutMinimum; // 最少输出代币数量 }

代码如下:

/// @inheritdoc ISwapRouter function exactInput(ExactInputParams memory params) external payable override checkDeadline(params.deadline) returns (uint256 amountOut) { address payer = msg.sender; // msg.sender pays for the first hop while (true) { bool hasMultiplePools = params.path.hasMultiplePools(); // the outputs of prior swaps become the inputs to subsequent ones params.amountIn = exactInputInternal( params.amountIn, hasMultiplePools ? address(this) : params.recipient, // for intermediate swaps, this contract custodies 0, SwapCallbackData({ path: params.path.getFirstPool(), // only the first pool in the path is necessary payer: payer }) ); // decide whether to continue or terminate if (hasMultiplePools) { payer = address(this); // at this point, the caller has paid params.path = params.path.skipToken(); } else { amountOut = params.amountIn; break; } } require(amountOut >= params.amountOutMinimum, 'Too little received'); }

在多池 swap 中,会按照 swap 路径,拆成多个单池 swap,循环进行,直到路径结束。如果是第一步 swap。payer 为合约调用方,否则 payer 为当前 SwapRouter 合约。

exactInputSingle方法负责单池交换,指定输入代币数量,尽可能多地获得输出代币。

参数如下,指定了输入代币地址和输出代币地址:

struct ExactInputSingleParams { address tokenIn; // 输入代币地址 address tokenOut; // 输出代币地址 uint24 fee; // 手续费费率 address recipient; // 接收者地址 uint256 deadline; // 过期的区块号 uint256 amountIn; // 输入代币数量 uint256 amountOutMinimum; // 最少输出代币数量 uint160 sqrtPriceLimitX96; // 限定价格,值为0则不限价 }

代码如下:

/// @inheritdoc ISwapRouter function exactInputSingle(ExactInputSingleParams calldata params) external payable override checkDeadline(params.deadline) returns (uint256 amountOut) { amountOut = exactInputInternal( params.amountIn, params.recipient, params.sqrtPriceLimitX96, SwapCallbackData({path: abi.encodePacked(params.tokenIn, params.fee, params.tokenOut), payer: msg.sender}) ); require(amountOut >= params.amountOutMinimum, 'Too little received'); }

实际调用 exactInputInternal,代码如下:

/// @dev Performs a single exact input swap function exactInputInternal( uint256 amountIn, address recipient, uint160 sqrtPriceLimitX96, SwapCallbackData memory data ) private returns (uint256 amountOut) { // allow swapping to the router address with address 0 if (recipient == address(0)) recipient = address(this); (address tokenIn, address tokenOut, uint24 fee) = data.path.decodeFirstPool(); bool zeroForOne = tokenIn < tokenOut; (int256 amount0, int256 amount1) = getPool(tokenIn, tokenOut, fee).swap( recipient, zeroForOne, amountIn.toInt256(), sqrtPriceLimitX96 == 0 ? (zeroForOne ? TickMath.MIN_SQRT_RATIO + 1 : TickMath.MAX_SQRT_RATIO - 1) : sqrtPriceLimitX96, abi.encode(data) ); return uint256(-(zeroForOne ? amount1 : amount0)); }

如果没有指定接收者地址,则默认为当前 SwapRouter 合约地址。这个目的是在多池交易中,将中间代币保存在 SwapRouter 合约中。

if (recipient == address(0)) recipient = address(this);

接着解析出交易路由信息 tokenIn,tokenOut 和 fee。并比较 tokenIn 和 tokenOut 的地址得到 zeroForOne,表示在当前交易池是否是 token0 交换 token1。

(address tokenIn, address tokenOut, uint24 fee) = data.path.decodeFirstPool(); bool zeroForOne = tokenIn < tokenOut;

最后调用交易池合约的 swap 方法,获取完成本次交换所需的 amount0 和 amount1,再根据 zeroForOne 返回 amountOut,进一步判断 amountOut 满足最少输出代币数量的要求,完成 swap。swap 方法相对复杂,放到后面专门讲。

指定输出代币数量

exactOutput 方法负责多池交换,指定 swap 路径以及输出代币数量,尽可能少地提供输入代币。

参数如下:

struct ExactOutputParams { bytes path; // swap 路径,可以解析成一个或多个交易池 address recipient; // 接收者地址 uint256 deadline; // 过期的区块号 uint256 amountOut; // 输出代币数量 uint256 amountInMaximum; // 最多输入代币数量 }

代码如下:

/// @inheritdoc ISwapRouter function exactOutput(ExactOutputParams calldata params) external payable override checkDeadline(params.deadline) returns (uint256 amountIn) { // it's okay that the payer is fixed to msg.sender here, as they're only paying for the "final" exact output // swap, which happens first, and subsequent swaps are paid for within nested callback frames exactOutputInternal( params.amountOut, params.recipient, 0, SwapCallbackData({path: params.path, payer: msg.sender}) ); amountIn = amountInCached; require(amountIn <= params.amountInMaximum, 'Too much requested'); amountInCached = DEFAULT_AMOUNT_IN_CACHED; }

在多池 swap 中,会按照 swap 路径,拆成多个单池 swap,循环进行,直到路径结束。如果是第一步 swap。payer 为合约调用方,否则 payer 为当前 SwapRouter 合约。

exactOutputSingle方法负责单池交换,指定输出代币数量,尽可能少地提供输入代币。

参数如下,指定了输入代币地址和输出代币地址:

struct ExactOutputSingleParams { address tokenIn; // 输入代币地址 address tokenOut; // 输出代币地址 uint24 fee; // 手续费费率 address recipient; // 接收者地址 uint256 deadline; // 过期的区块号 uint256 amountOut; // 输出代币数量 uint256 amountInMaximum; // 最多输入代币数量 uint160 sqrtPriceLimitX96; // 限定价格,值为0则不限价 }

代码如下:

/// @inheritdoc ISwapRouter function exactOutputSingle(ExactOutputSingleParams calldata params) external payable override checkDeadline(params.deadline) returns (uint256 amountIn) { // avoid an SLOAD by using the swap return data amountIn = exactOutputInternal( params.amountOut, params.recipient, params.sqrtPriceLimitX96, SwapCallbackData({path: abi.encodePacked(params.tokenOut, params.fee, params.tokenIn), payer: msg.sender}) ); require(amountIn <= params.amountInMaximum, 'Too much requested'); // has to be reset even though we don't use it in the single hop case amountInCached = DEFAULT_AMOUNT_IN_CACHED; }

实际调用 exactOutputInternal,代码如下:

/// @dev Performs a single exact output swap function exactOutputInternal( uint256 amountOut, address recipient, uint160 sqrtPriceLimitX96, SwapCallbackData memory data ) private returns (uint256 amountIn) { // allow swapping to the router address with address 0 if (recipient == address(0)) recipient = address(this); (address tokenOut, address tokenIn, uint24 fee) = data.path.decodeFirstPool(); bool zeroForOne = tokenIn < tokenOut; (int256 amount0Delta, int256 amount1Delta) = getPool(tokenIn, tokenOut, fee).swap( recipient, zeroForOne, -amountOut.toInt256(), sqrtPriceLimitX96 == 0 ? (zeroForOne ? TickMath.MIN_SQRT_RATIO + 1 : TickMath.MAX_SQRT_RATIO - 1) : sqrtPriceLimitX96, abi.encode(data) ); uint256 amountOutReceived; (amountIn, amountOutReceived) = zeroForOne ? (uint256(amount0Delta), uint256(-amount1Delta)) : (uint256(amount1Delta), uint256(-amount0Delta)); // it's technically possible to not receive the full output amount, // so if no price limit has been specified, require this possibility away if (sqrtPriceLimitX96 == 0) require(amountOutReceived == amountOut); }

跟 exactInputInternal 的逻辑几乎完全一致,除了因为指定输出代币数量,调用交易池合约 swap 方法使用 -amountOut.toInt256() 作为参数。

(int256 amount0Delta, int256 amount1Delta) = getPool(tokenIn, tokenOut, fee).swap( recipient, zeroForOne, -amountOut.toInt256(), sqrtPriceLimitX96 == 0 ? (zeroForOne ? TickMath.MIN_SQRT_RATIO + 1 : TickMath.MAX_SQRT_RATIO - 1) : sqrtPriceLimitX96, abi.encode(data) );

返回的 amount0Delta 和 amount1Delta 为完成本次 swap 所需的 token0 数量和实际输出的 token1 数量,进一步判断 amountOut 满足最少输出代币数量的要求,完成 swap。

swap

一个通常的 V3 交易池存在很多互相重叠的价格区间的头寸,如下图所示:

每个交易池都会跟踪当前的价格,以及所有包含现价的价格区间提供的总流动性 liquidity。在每个区间的边界的 tick 上记录下 \Delta{L},当价格波动,穿过某个 tick 时,会根据价格波动方向进行流动性的增加或者减少。例如价格从左到右穿过区间,当穿过区间的第一个 tick 时,流动性需要增加 \Delta{L},穿出最后一个 tick 时,流动性需要减少 \Delta{L},中间的 tick 则流动性保持不变。

在一个 tick 内的流动性是常数, swap 公式如下:

P_{current}是 swap 前的价格, P_{target}是 swap 后的价格,L 是 tick 内的流动性。

从上面公式,可以通过输入 token1 的数量 \Delta{y}推导出目标价格 P_{target},进而推导出输出 token0 的数量 \Delta{x};或者通过输入 token0 的数量 \Delta{x}推导出目标价格 P_{target},进而推导出输出 token1 的数量 \Delta{y}。

如果是跨 tick 交易则需要拆解成多个 tick 内的交易:如果当前 tick 的流动性不能满足要求,价格会移动到当前区间的边界处。此时,使离开的区间休眠,并激活下一个区间。并且会开始下一个循环并且寻找下一个有流动性的 tick,直到用户需求的数量被满足。

讲完理论,回到代码。swap 方法是交易对 swap 最核心的方法,也是最复杂的方法。

参数为:

- recipient:接收者的地址;

- zeroForOne:如果从 token0 交换 token1 则为 true,从 token1 交换 token0 则为 false;

- amountSpecified:指定的代币数量,指定输入的代币数量则为正数,指定输出的代币数量则为负数;

- sqrtPriceLimitX96:限定价格,如果从 token0 交换 token1 则限定价格下限,从 token1 交换 token0 则限定价格上限;

- data:回调参数。

代码为:

/// @inheritdoc IUniswapV3PoolActions function swap( address recipient, bool zeroForOne, int256 amountSpecified, uint160 sqrtPriceLimitX96, bytes calldata data ) external override noDelegateCall returns (int256 amount0, int256 amount1) { require(amountSpecified != 0, 'AS'); Slot0 memory slot0Start = slot0; require(slot0Start.unlocked, 'LOK'); require( zeroForOne ? sqrtPriceLimitX96 < slot0Start.sqrtPriceX96 && sqrtPriceLimitX96 > TickMath.MIN_SQRT_RATIO : sqrtPriceLimitX96 > slot0Start.sqrtPriceX96 && sqrtPriceLimitX96 < TickMath.MAX_SQRT_RATIO, 'SPL' ); slot0.unlocked = false; SwapCache memory cache = SwapCache({ liquidityStart: liquidity, blockTimestamp: _blockTimestamp(), feeProtocol: zeroForOne ? (slot0Start.feeProtocol % 16) : (slot0Start.feeProtocol >> 4), secondsPerLiquidityCumulativeX128: 0, tickCumulative: 0, computedLatestObservation: false }); bool exactInput = amountSpecified > 0; SwapState memory state = SwapState({ amountSpecifiedRemaining: amountSpecified, amountCalculated: 0, sqrtPriceX96: slot0Start.sqrtPriceX96, tick: slot0Start.tick, feeGrowthGlobalX128: zeroForOne ? feeGrowthGlobal0X128 : feeGrowthGlobal1X128, protocolFee: 0, liquidity: cache.liquidityStart }); // continue swapping as long as we haven't used the entire input/output and haven't reached the price limit while (state.amountSpecifiedRemaining != 0 && state.sqrtPriceX96 != sqrtPriceLimitX96) { StepComputations memory step; step.sqrtPriceStartX96 = state.sqrtPriceX96; (step.tickNext, step.initialized) = tickBitmap.nextInitializedTickWithinOneWord( state.tick, tickSpacing, zeroForOne ); // ensure that we do not overshoot the min/max tick, as the tick bitmap is not aware of these bounds if (step.tickNext < TickMath.MIN_TICK) { step.tickNext = TickMath.MIN_TICK; } else if (step.tickNext > TickMath.MAX_TICK) { step.tickNext = TickMath.MAX_TICK; } // get the price for the next tick step.sqrtPriceNextX96 = TickMath.getSqrtRatioAtTick(step.tickNext); // compute values to swap to the target tick, price limit, or point where input/output amount is exhausted (state.sqrtPriceX96, step.amountIn, step.amountOut, step.feeAmount) = SwapMath.computeSwapStep( state.sqrtPriceX96, (zeroForOne ? step.sqrtPriceNextX96 < sqrtPriceLimitX96 : step.sqrtPriceNextX96 > sqrtPriceLimitX96) ? sqrtPriceLimitX96 : step.sqrtPriceNextX96, state.liquidity, state.amountSpecifiedRemaining, fee ); if (exactInput) { state.amountSpecifiedRemaining -= (step.amountIn + step.feeAmount).toInt256(); state.amountCalculated = state.amountCalculated.sub(step.amountOut.toInt256()); } else { state.amountSpecifiedRemaining += step.amountOut.toInt256(); state.amountCalculated = state.amountCalculated.add((step.amountIn + step.feeAmount).toInt256()); } // if the protocol fee is on, calculate how much is owed, decrement feeAmount, and increment protocolFee if (cache.feeProtocol > 0) { uint256 delta = step.feeAmount / cache.feeProtocol; step.feeAmount -= delta; state.protocolFee += uint128(delta); } // update global fee tracker if (state.liquidity > 0) state.feeGrowthGlobalX128 += FullMath.mulDiv(step.feeAmount, FixedPoint128.Q128, state.liquidity); // shift tick if we reached the next price if (state.sqrtPriceX96 == step.sqrtPriceNextX96) { // if the tick is initialized, run the tick transition if (step.initialized) { // check for the placeholder value, which we replace with the actual value the first time the swap // crosses an initialized tick if (!cache.computedLatestObservation) { (cache.tickCumulative, cache.secondsPerLiquidityCumulativeX128) = observations.observeSingle( cache.blockTimestamp, 0, slot0Start.tick, slot0Start.observationIndex, cache.liquidityStart, slot0Start.observationCardinality ); cache.computedLatestObservation = true; } int128 liquidityNet = ticks.cross( step.tickNext, (zeroForOne ? state.feeGrowthGlobalX128 : feeGrowthGlobal0X128), (zeroForOne ? feeGrowthGlobal1X128 : state.feeGrowthGlobalX128), cache.secondsPerLiquidityCumulativeX128, cache.tickCumulative, cache.blockTimestamp ); // if we're moving leftward, we interpret liquidityNet as the opposite sign // safe because liquidityNet cannot be type(int128).min if (zeroForOne) liquidityNet = -liquidityNet; state.liquidity = LiquidityMath.addDelta(state.liquidity, liquidityNet); } state.tick = zeroForOne ? step.tickNext - 1 : step.tickNext; } else if (state.sqrtPriceX96 != step.sqrtPriceStartX96) { // recompute unless we're on a lower tick boundary (i.e. already transitioned ticks), and haven't moved state.tick = TickMath.getTickAtSqrtRatio(state.sqrtPriceX96); } } // update tick and write an oracle entry if the tick change if (state.tick != slot0Start.tick) { (uint16 observationIndex, uint16 observationCardinality) = observations.write( slot0Start.observationIndex, cache.blockTimestamp, slot0Start.tick, cache.liquidityStart, slot0Start.observationCardinality, slot0Start.observationCardinalityNext ); (slot0.sqrtPriceX96, slot0.tick, slot0.observationIndex, slot0.observationCardinality) = ( state.sqrtPriceX96, state.tick, observationIndex, observationCardinality ); } else { // otherwise just update the price slot0.sqrtPriceX96 = state.sqrtPriceX96; } // update liquidity if it changed if (cache.liquidityStart != state.liquidity) liquidity = state.liquidity; // update fee growth global and, if necessary, protocol fees // overflow is acceptable, protocol has to withdraw before it hits type(uint128).max fees if (zeroForOne) { feeGrowthGlobal0X128 = state.feeGrowthGlobalX128; if (state.protocolFee > 0) protocolFees.token0 += state.protocolFee; } else { feeGrowthGlobal1X128 = state.feeGrowthGlobalX128; if (state.protocolFee > 0) protocolFees.token1 += state.protocolFee; } (amount0, amount1) = zeroForOne == exactInput ? (amountSpecified - state.amountSpecifiedRemaining, state.amountCalculated) : (state.amountCalculated, amountSpecified - state.amountSpecifiedRemaining); // do the transfers and collect payment if (zeroForOne) { if (amount1 < 0) TransferHelper.safeTransfer(token1, recipient, uint256(-amount1)); uint256 balance0Before = balance0(); IUniswapV3SwapCallback(msg.sender).uniswapV3SwapCallback(amount0, amount1, data); require(balance0Before.add(uint256(amount0)) <= balance0(), 'IIA'); } else { if (amount0 < 0) TransferHelper.safeTransfer(token0, recipient, uint256(-amount0)); uint256 balance1Before = balance1(); IUniswapV3SwapCallback(msg.sender).uniswapV3SwapCallback(amount0, amount1, data); require(balance1Before.add(uint256(amount1)) <= balance1(), 'IIA'); } emit Swap(msg.sender, recipient, amount0, amount1, state.sqrtPriceX96, state.liquidity, state.tick); slot0.unlocked = true; }

整体逻辑由一个 while 循环组成,将 swap 过程分解成多个小步骤,一点点的调整当前的 tick,直到满足用户所需的交易量或者价格触及限定价格(此时会部分成交)。

while (state.amountSpecifiedRemaining != 0 && state.sqrtPriceX96 != sqrtPriceLimitX96) {

使用 `tickBitmap.nextInitializedTickWithinOneWord`` 来找到下一个已初始化的 tick

(step.tickNext, step.initialized) = tickBitmap.nextInitializedTickWithinOneWord( state.tick, tickSpacing, zeroForOne );

使用 SwapMath.computeSwapStep 进行 tick 内的 swap。这个方法会计算出当前区间可以满足的输入数量 amountIn,如果它比 amountRemaining 要小,我们会说现在的区间不能满足整个交易,因此下一个 sqrtPriceX96 就是当前区间的上界/下界,也就是说,我们消耗完了整个区间的流动性。如果 amountIn 大于 amountRemaining,我们计算的 sqrtPriceX96 仍然在现在区间内。

// compute values to swap to the target tick, price limit, or point where input/output amount is exhausted (state.sqrtPriceX96, step.amountIn, step.amountOut, step.feeAmount) = SwapMath.computeSwapStep( state.sqrtPriceX96, (zeroForOne ? step.sqrtPriceNextX96 < sqrtPriceLimitX96 : step.sqrtPriceNextX96 > sqrtPriceLimitX96) ? sqrtPriceLimitX96 : step.sqrtPriceNextX96, state.liquidity, state.amountSpecifiedRemaining, fee );

保存本次交易的 amountIn 和 amountOut:

- 如果是指定输入代币数量。amountSpecifiedRemaining 表示剩余可用输入代币数量,amountCalculated 表示已输出代币数量(以负数表示);

- 如果是指定输出代币数量。amountSpecifiedRemaining 表示剩余需要输出的代币数量(初始为负值,因此每次交换后需要加上 step.amountOut,直到为 0),amountCalculated 表示已使用的输入代币数量。

if (exactInput) { state.amountSpecifiedRemaining -= (step.amountIn + step.feeAmount).toInt256(); state.amountCalculated = state.amountCalculated.sub(step.amountOut.toInt256()); } else { state.amountSpecifiedRemaining += step.amountOut.toInt256(); state.amountCalculated = state.amountCalculated.add((step.amountIn + step.feeAmount).toInt256()); }

如果本次 swap 后的价格达到目标价格,如果该 tick 已经初始化,则通过 ticks.cross 方法穿越该 tick,返回新增的净流动性 liquidityNet 更新可用流动性 state.liquidity,移动当前 tick 到下一个 tick。

如果本次 swap 后的价格达到目标价格,但是又不等于初始价格,即表示此时 swap 结束,使用 swap 后的价格计算最新的 tick 值。

if (state.sqrtPriceX96 == step.sqrtPriceNextX96) { // if the tick is initialized, run the tick transition if (step.initialized) { // check for the placeholder value, which we replace with the actual value the first time the swap // crosses an initialized tick if (!cache.computedLatestObservation) { (cache.tickCumulative, cache.secondsPerLiquidityCumulativeX128) = observations.observeSingle( cache.blockTimestamp, 0, slot0Start.tick, slot0Start.observationIndex, cache.liquidityStart, slot0Start.observationCardinality ); cache.computedLatestObservation = true; } int128 liquidityNet = ticks.cross( step.tickNext, (zeroForOne ? state.feeGrowthGlobalX128 : feeGrowthGlobal0X128), (zeroForOne ? feeGrowthGlobal1X128 : state.feeGrowthGlobalX128), cache.secondsPerLiquidityCumulativeX128, cache.tickCumulative, cache.blockTimestamp ); // if we're moving leftward, we interpret liquidityNet as the opposite sign // safe because liquidityNet cannot be type(int128).min if (zeroForOne) liquidityNet = -liquidityNet; state.liquidity = LiquidityMath.addDelta(state.liquidity, liquidityNet); } state.tick = zeroForOne ? step.tickNext - 1 : step.tickNext; } else if (state.sqrtPriceX96 != step.sqrtPriceStartX96) { // recompute unless we're on a lower tick boundary (i.e. already transitioned ticks), and haven't moved state.tick = TickMath.getTickAtSqrtRatio(state.sqrtPriceX96); }

重复上述步骤,直到 swap 完全结束。

完成 swap 后,更新 slot0 的状态和全局流动性。

// update tick and write an oracle entry if the tick change if (state.tick != slot0Start.tick) { (uint16 observationIndex, uint16 observationCardinality) = observations.write( slot0Start.observationIndex, cache.blockTimestamp, slot0Start.tick, cache.liquidityStart, slot0Start.observationCardinality, slot0Start.observationCardinalityNext ); (slot0.sqrtPriceX96, slot0.tick, slot0.observationIndex, slot0.observationCardinality) = ( state.sqrtPriceX96, state.tick, observationIndex, observationCardinality ); } else { // otherwise just update the price slot0.sqrtPriceX96 = state.sqrtPriceX96; } // update liquidity if it changed if (cache.liquidityStart != state.liquidity) liquidity = state.liquidity;

最后,计算本次 swap 需要的具体 amount0 和 amount1,调用 IUniswapV3SwapCallback 接口。在回调之前已经把输出的 token 发送给了 recipient。

// do the transfers and collect payment if (zeroForOne) { if (amount1 < 0) TransferHelper.safeTransfer(token1, recipient, uint256(-amount1)); uint256 balance0Before = balance0(); IUniswapV3SwapCallback(msg.sender).uniswapV3SwapCallback(amount0, amount1, data); require(balance0Before.add(uint256(amount0)) <= balance0(), 'IIA'); } else { if (amount0 < 0) TransferHelper.safeTransfer(token0, recipient, uint256(-amount0)); uint256 balance1Before = balance1(); IUniswapV3SwapCallback(msg.sender).uniswapV3SwapCallback(amount0, amount1, data); require(balance1Before.add(uint256(amount1)) <= balance1(), 'IIA'); }

IUniswapV3SwapCallback 的实现在 periphery 仓库的 SwapRouter.sol 中,负责支付输入的 token。

/// @inheritdoc IUniswapV3SwapCallback function uniswapV3SwapCallback( int256 amount0Delta, int256 amount1Delta, bytes calldata _data ) external override { require(amount0Delta > 0 || amount1Delta > 0); // swaps entirely within 0-liquidity regions are not supported SwapCallbackData memory data = abi.decode(_data, (SwapCallbackData)); (address tokenIn, address tokenOut, uint24 fee) = data.path.decodeFirstPool(); CallbackValidation.verifyCallback(factory, tokenIn, tokenOut, fee); (bool isExactInput, uint256 amountToPay) = amount0Delta > 0 ? (tokenIn < tokenOut, uint256(amount0Delta)) : (tokenOut < tokenIn, uint256(amount1Delta)); if (isExactInput) { pay(tokenIn, data.payer, msg.sender, amountToPay); } else { // either initiate the next swap or pay if (data.path.hasMultiplePools()) { data.path = data.path.skipToken(); exactOutputInternal(amountToPay, msg.sender, 0, data); } else { amountInCached = amountToPay; tokenIn = tokenOut; // swap in/out because exact output swaps are reversed pay(tokenIn, data.payer, msg.sender, amountToPay); } } }

至此,完成了整体 swap 流程。